Of the 50 U.S. counties with the risk for distressed properties, 31 are concentrated in four states, led by Florida, an Attom Data Solutions analysis found.

Processing Content

Florida is the home of 12 of those counties, with the No. 1 most at risk locale in the nation being Charlotte County. California was next with nine, while Illinois and New Jersey had five each. The results were similar to

After Charlotte County, Butte County in California was next, followed by Charles County, Maryland, Shasta County, California and Cumberland County, New Jersey.

The riskiest markets have similar characteristics, namely

“While home prices have eased slightly from last summer’s record highs, affordability remains a challenge in much of the country,” Attom CEO Rob Barber said in a press release. “The greatest risk remains in counties where unemployment rates are above 5% and homes are being foreclosed at greater rates.”

Besides unemployment and the percentage of homes facing foreclosure, other considerations included the share of seriously underwater mortgages, plus the percentage of the average local wage needed to pay for major home ownership expenses for a median priced home.

The list was created from an analysis of 580 U.S. counties with sufficient data available for the first quarter.

At the other end of the spectrum, of the 50 counties with the least risk, nine were in Tennessee, five each in Virginia and Wisconsin and four in Michigan.

The five least risky counties were Chittenden County, Vermont; Rutherford County, Tennessee; Arlington County, Virginia; Tippecanoe County, Indiana; and Cumberland County, Maine.

Those counties were not notably more affordable than others, Attom pointed out. But each benefited from some of the lowest unemployment and best foreclosure rates in the country, along with a low share of underwater mortgages.

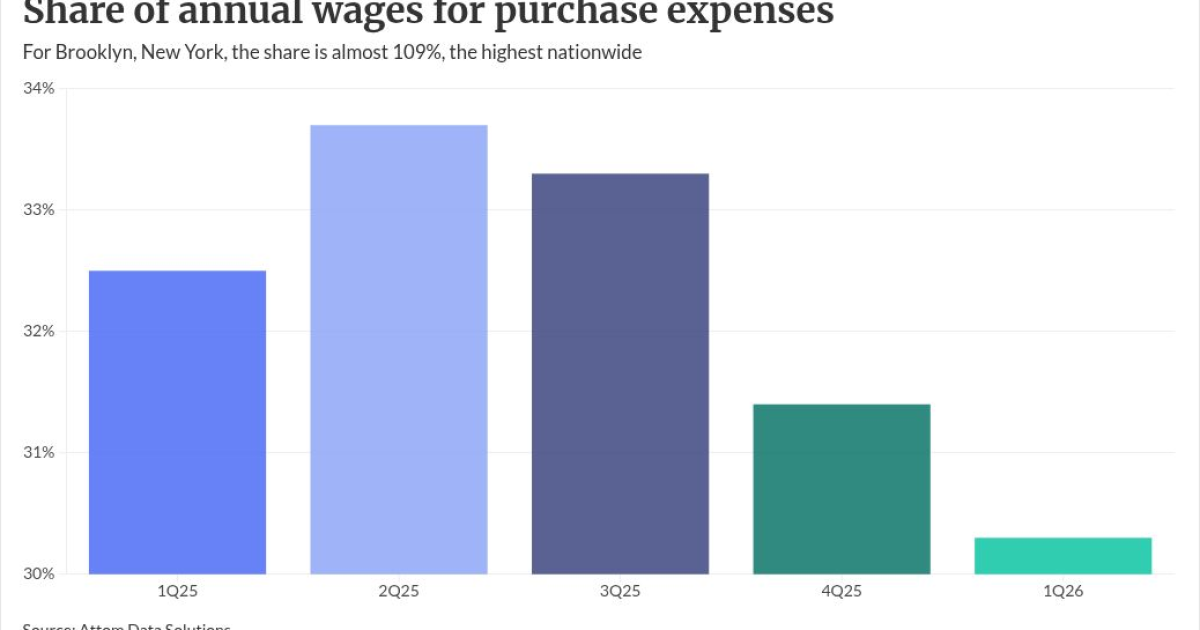

The report found the national median home sales price in the first quarter totaled $360,000. This would need 30.3% of the typical American worker’s annual wage to afford major monthly purchase expenses. This is an improvement from one year ago, when the share was 32.5%.

Kings County, otherwise known as the borough of Brooklyn, expenses for a median priced home in this part of New York City consumed 108.6% of a typical resident’s wages. The next four counties on the list were all in California: Santa Cruz, 97.1%; Marin, 91.1%; San Luis Obispo, 89.7%; and Orange, 98.1%.

Louisiana was the state whose jurisdictions, known as parishes, occupied the top of the listings most properties

The Attom report said one out of every 1,211 homes nationwide were in the process of foreclosure. The highest rate was in Liberty County, Texas, one-in-every-55 homes. Baltimore was second, at one-in-every 294 homes.

A recent report from Cotality noted

Its data, which measures metro areas, had Odessa, Texas, in a different part of the state, as the area with the largest increase in the serious delinquent rate, a year-over-year gain of one percentage point. The overall delinquency rate for Odessa increased 1.1 percentage points, trailing Pine Bluff, Arkansas, up 1.5 percentage points.

Publisher: Source link