Miruna-Daniela Ivan

The widespread practice of financial institution to re-use securities received as collateral plays a key role in the repurchase agreement (repo) market functioning. By increasing the availability of securities which can be used as collateral, collateral re-use lowers funding costs under normal market conditions, allowing collateral to flow to where it is most needed. But this activity may amplify the risk of delivery failures and increase volatility in repo rates during periods of market stress. This article explores the level of collateral re-use in the gilt repo market, applying algorithms from academic literature to the Bank’s Sterling Money Market Data, and provides supporting evidence of collateral re-use procyclicality, and its positive relation to repo rates volatility.

What is collateral re-use, who re-uses collateral and what motivates it?

The re-use of collateral refers to the practice of financial institutions to re-use securities received as collateral, generally in securities financing transactions (SFTs) (ie, repo and securities-lending agreements), to finance secured lending or to source securities to short sell (FSB (2017)). This practice is prevalent in the repo market given that repo dealers play a crucial role in facilitating the flow of cash and securities around the financial system (Hempel et al (2024)). Collateral is typically re-used by large dealer banks for their market making activity, and by hedge funds who are looking to source specific bonds (eg, specific collateral) for their relative value trading strategies. Increased demand for a specific bond may arise when that bond becomes the cheapest-to-deliver in the futures market.

Scarcity of specific assets is a key driver of collateral re-use. Limited availability of specific government bond securities for market participants (eg, arising when central bank asset purchase programmes have significant holdings of those securities) can interact with the short-selling activity of hedge funds and the market making activity of dealers. These interactions can have significant and persistent effects on the liquidity of core government bond markets such as the gilt market. Hence, financial institutions tend to adjust to collateral scarcity by increasing the re-use of collateral.

How does collateral re-use work in practice?

When collateral is being re-used, flows tend to involve non-bank financial institutions (NBFIs) and large dealer banks (‘prime brokers’) that specialise in collateral intermediation. The NBFIs active are typically hedge funds on the supply side of collateral, and money market funds and asset managers on the demand side. By posting collateral for re-use to their prime brokers in repo transactions, hedge funds become more leveraged. In turn, dealer banks finance their secured lending by posting the collateral received to cash investors such as money market funds or asset managers. Figure 1 provides an example: a hedge fund finances a relative value trading strategy through a repo agreement, posting quantity Q of Bond A worth £100 to a dealer bank. Assuming the repo transaction is at zero haircuts, the hedge fund receives the market value of Bond A (£100), with an agreement to repurchase the bond at a future date. In turn, the dealer bank finances this secured lending by engaging in a repo transaction with a money market fund (MMF) and/or an asset manager re-using the securities received from the hedge fund. The dealer bank could post Q/2 of Bond A to the MMF, receiving the market value of Q/2 of Bond A (£50), and Q/2 of Bond A to the asset manager, receiving £50. The maturity date of the re-used transactions must be not later than the maturity date of the initial transaction, so that the dealer bank is able to repurchase Q/2 of Bond A from the MMF and asset manager, and return the collateral pledged to the hedge fund.

Figure 1: Collateral flows involving non-bank financial institutions and large dealer banks (a)

(a) Q refers to the quantity of collateral transferred between large dealer banks and NBFIs.

Why do we care?

The re-use of collateral has clear benefits for liquidity in modern financial markets, since collateral received in a reverse repo transaction can be re-used to support other financial transactions. Through this practice, market participants increase the availability of safe assets, lowering the cost of capital, to the benefit of the real economy. Despite this, collateral re-use has exacerbated financial crises in the past by facilitating the build-up of delivery failures and high bond and repo volatility (Capel and Levels (2014); Moench et al (2020); and Brumm et al (2018)). Uncertainty about the extent to which the collateral posted has been re-used and its treatment in the event of bankruptcy are also contributing factors to systemic liquidity risks related to the re-use of client assets, as noted by FSB (2013) and highlighted in Infante et al (2018). As predicted by Brunnermeier and Pedersen (2009), declines in liquidity in one market can spill over into other markets because traders’ ability to borrow becomes constrained. These liquidity spirals are driven by the bankruptcy of a prime broker which re-used the collateral received from its client to secure other transactions.

How widespread is collateral re-use in the gilt repo market?

The average collateral re-use in the gilt repo market was about 3.5% over the sample period (January 2017 to April 2023). In other words, 3.5% of the outstanding gilt repo was secured with re-used collateral. The collateral re-use is the ratio of the market value of the re-used gilt securities to the gilt repo outstanding. As depicted by Chart 1, the collateral re-use was the highest between March 2020 and end of 2021 (~3.2% to 4.2%), when the Monetary Policy Committee (MPC) increased the stock of asset purchases by £450 billion (most of which were UK government bonds). Specific asset scarcity has subsided to some extent since the end of 2022, when the MPC agreed to reduce the stock of UK government bond purchases. Collateral re-use increased slightly around the March 2020 ‘dash for cash’ and during the September 2022 liability-driven investment (LDI) market disruption, providing some evidence of collateral re-use procyclicality in the gilt repo market.

Chart 1: Trends in collateral re-use and safe asset scarcity (a) (b)

Sources: Asset Purchase Facility: Gilt Sales, Sterling Money Market Data (SMMD) and Bank calculations.

(a) The sample period is January 2017 to April 2023 at monthly frequency.

(b) The collateral re-use is computed as the ratio of the market value of gilts received by financial institutions, that is re-used at a point in time, to the overall gilt repo activity. The re-use rate does not account for the pool of eligible gilt securities.

The risk behind the collateral re-use

The re-use of collateral alleviates traders funding liquidity needs in normal market conditions, as noted by Monnet (2011). However, excessive collateral re-use could also represent an important risk channel in times of market stress, as it creates collateral chains (ie, multiple transactions are collateralised by the same type of security), which may amplify the risk of specific collateral delivery failures during periods of market stress. Notably, gilt specific securities serving as collateral in repo account for over 85% of the total repo stock outstanding, as observed in UK Securities Financing Transaction Regulation data.

Elevated collateral re-use may amplify initial idiosyncratic shocks by increasing interconnectedness among market participants and subsequently, the risk of contagion and settlement fails. The mechanism operates as follows. In response to an idiosyncratic shock, market participants tend to hoard liquidity (eg, high quality securities) in anticipation of margin calls for other transactions, by tapping repo markets (Gai et al (2011); and Bakoush et al (2019)). When collateral re-use is high, precautionary hoarding of securities further constrains their availability. This is because counterparties along the collateral (re-use) chain may struggle to return the specific securities, increasing the risk of specific collateral delivery failures.

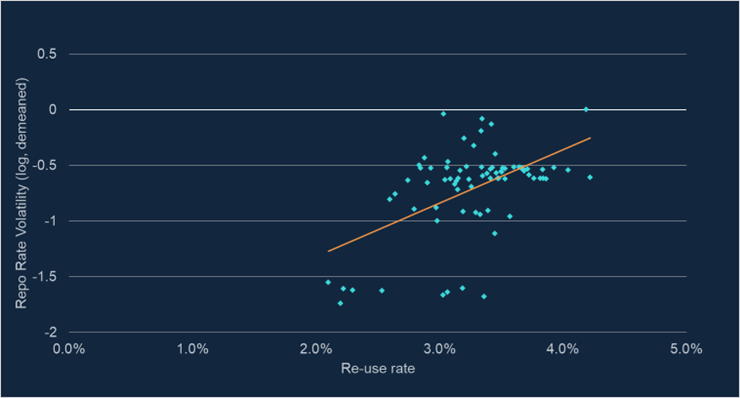

In line with Moench et al (2020), I find that that the volatility of repo rates in the gilt market is positively associated with collateral re-use (ie, correlation coefficient of ~53%) (Chart 2). These findings provide supporting evidence that elevated collateral re-use may be associated with increased volatility in the gilt repo market and highlight the need for further research into the unintended consequences of collateral re-use. Appropriately monitoring collateral re-use at the global level is especially important for building a clearer understanding of global collateral re-use activities in the securities financing markets. These insights will also inform our macroprudential surveillance, enhancing our ability to detect and mitigate interconnectedness-related vulnerabilities that could pose systemic risks or intensify market disruptions.

Chart 2: Collateral re-use and repo rate volatility (a) (b) (c)

Sources: SMMD and Bank calculations.

(a) The sample period is January 2017 to April 2023 at monthly frequency.

(b) The collateral re-use is computed as the proportion of total collateral received by financial institutions, that is re-used at a point in time.

(c) The repo rate volatility is measured as the standard deviation of repo rates for each month. For visualisation, we demean the volatility measure.

Miruna-Daniela Ivan works in the Bank’s Market-Based Finance Division.

If you want to get in touch, please email us at [email protected] or leave a comment below.

Comments will only appear once approved by a moderator, and are only published where a full name is supplied. Bank Underground is a blog for Bank of England staff to share views that challenge – or support – prevailing policy orthodoxies. The views expressed here are those of the authors, and are not necessarily those of the Bank of England, or its policy committees.

Share the post “Collateral re-use: unveiling the risk of delivery failures and higher volatility in the repo market”

Publisher: Source link

{kind=link}

{kind=link}

{kind=link}

{kind=link}