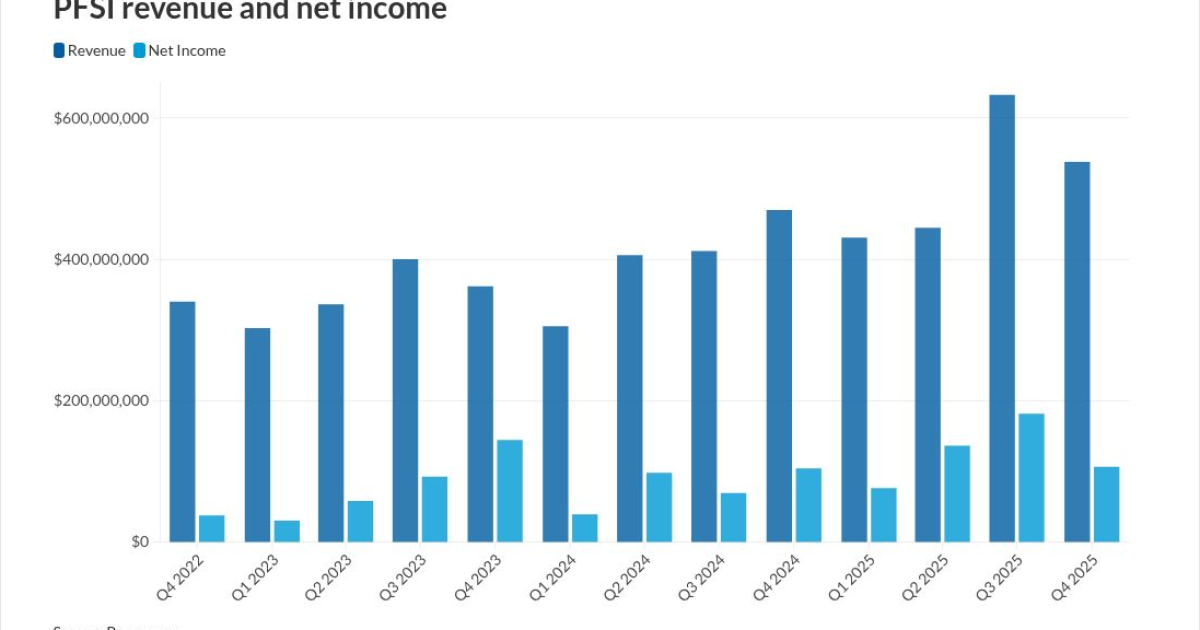

PennyMac Financial Services fourth quarter earnings were affected by the lower interest rate environment in the quarter, coming in higher year-over-year but reduced versus the linked quarter.

Processing Content

PFSI reported $106.8 million in net income for the quarter and $501.1 million for the year.

Earnings per share for the quarter under generally accepted accounting principles were $1.97, compared with a $3.26 Standard & Poor’s consensus estimate

The company’s stock was down almost 20% in after hours trading with some investors buying the dip, according to a BTIG report distributed late Thursday.

Competition in lending impacted margins and prepayments in excess of broader industry expectations challenged the company during the period, but its results have been improving in the first quarter, executives said during an earnings call.

“We’ve taken strategic and targeted actions to drive improvements over the course of this year,” Chairman and CEO David Spector said.

Origination and servicing results

The production segment brought in $127.3 million in pretax income compared to $123 million a quarter earlier and $78 million in 4Q24. Meanwhile, servicing generated $37 million in net income for the quarter compared to $157 million the previous fiscal period and $87 million a year earlier.

Falling rate environments like the fourth quarter’s tend to benefit lending while challenging servicing with runoff as customers become more active seeking new loans. Rising rates usually benefit servicing but challenge production. This is in part because mortgage servicing rights are generally marked-to-market.

Servicing does still have benefits in a falling rate environment when it comes to retaining or recapturing customers at risk of refinancing or getting a new loan from a different company.

“While production segment income was approximately double the levels reported in the first two quarters of this year, the growth from the third quarter to the fourth quarter did not offset the runoff of the portfolio,” Spector said.

“We are positioning ourselves to better capture the significant opportunities presented by lower mortgage rates and further increase production income in comparison to MSR runoff,” he added.

Pennymac’s correspondent rate locks and direct lending interest-rate lock commitments totaled $42.8 billion compared with $33.1 billion a year ago and $38.9 billion in 3Q25.

The 4Q25 total for loan acquisitions and originations was $42.2 billion compared to $36.5 billion in the third quarter and $35.7 billion a year earlier.

How the company is handling margin compression

“The contribution from higher volumes in the channel was largely offset by lower margins from increased competition,” Chief Financial Officer Dan Perotti noted on the call.

Spector said the company has taken steps to address this by shifting its business mix more toward higher margin direct lending channels.

“This is driving our expectations for production segment income in the first quarter to be higher,” he said.

Publisher: Source link