Philippe Bracke, Matt Everitt, Martina Fazio and Alexandra Varadi

The Bank of England Agenda for Research (BEAR) sets the key areas for new research at the Bank over the coming years. This post is an example of issues considered under the Macroeconomic Environment Theme which focuses on the changing inflation dynamics and unfolding structural change faced by monetary policy makers.

How do mortgagors adjust spending, savings and debt during monetary tightening? In a recent paper, we explore this question using a novel data set on household transactions and mortgage records. About 30% of households used mortgage flexibility when facing higher borrowing costs since late 2021, as their fixed-rate contracts ended. Some extended repayment periods to lower monthly payments, while others increased borrowing by extracting housing equity – leveraging nominal price gains since the pandemic – to sustain spending and reduce unsecured debt. Those unable or unwilling to use mortgage flexibility, cut spending significantly. We thus document the dual role of mortgage flexibility at refinancing: it helps smooth consumption aiding financial resilience; but it may also dampen monetary policy transmission for some households.

The mortgage market channel of monetary policy transmission

In the UK, long-term fixed-rate mortgage contracts are relatively uncommon and refinancing occurs every 2–5 years to avoid rolling onto much more expensive standard variable rates. Since a third of the UK population has a mortgage, and refinancing is frequent, the pass-through of monetary policy to the mortgage market is stronger than in countries with longer fixed-term contracts, such as the US. Thus, the mortgage market is an especially important channel of transmission of monetary policy in the UK. When interest rates rise, mortgage payments increase too, directly reducing households’ disposable income (the ‘cash-flow channel’). Although many homeowners hold substantial wealth in housing, this wealth is illiquid and cannot be accessed during the fixed-rate period of the mortgage. UK lenders impose punitive early repayment charges for changing loan terms, withdrawing home equity or selling properties before the end of the fixed-term contract.

We show that at the refinancing event, about one-in-three households rely on two key dimensions of mortgage flexibility to mitigate the impact of the cash-flow channel. First, rising property values between refinancing events improve homeowners’ wealth, allowing them to increase borrowing against their property via home equity extraction. This collateral-driven borrowing is associated with higher spending and unsecured-debt repayments. Second, lengthening mortgage repayment periods – known as ‘mortgage term extensions’ in the UK – helps households reduce monthly mortgage repayments. They are sometimes used in combination with home equity withdrawals to lower debt burdens from the additional borrowing. Table A summarises the impact that these mortgage flexibility measures have on mortgage holders, which we explore in this post.

Table A: Mortgage flexibility measures and their impact on mortgage repayments

| Impact on monthly repayments | Collateral-driven borrowing | |

| Equity extraction | Increase | Yes – lump sum at refinancing |

| Term extension | Decrease | No – additional capital borrowed |

| Both | Ambiguous (the two will offset each other) | Yes – lump sum at refinancing |

Identifying the effect of rising mortgage rates on household spending and debt behaviour

To identify the effect of rising mortgage rates, we exploit four unique features of the UK mortgage market and a novel matched data set.

First, we exploit the quasi-exogenous timing of refinancing in the UK. Cloyne et al (2019) shows that in the UK, when households choose a fixed-term contract length for their mortgage rate, they are unable to perfectly foresee the macroeconomic conditions they will face when the fixed-rate contractual period ends. As such, the timing of refinancing onto a new fixed-rate contract is independent from current households’ characteristics. Our method for causal identification follows Di Maggio et al (2017). We use a difference-in-difference approach to compare households refinancing during the tightening cycle (June 2022 to December 2023) – our treated units – to household who refinanced earlier (before December 2021) – our control units. We control for demand-driven factors that may affect mortgage rates at refinancing independently of monetary policy tightening, such as loan to values (as a proxy for borrower riskiness), income, time-invariant household-specific characteristics and broader time-varying economic shocks, like inflation. The residual captures household responses that are due specifically to the hiking cycle.

Second, we exploit the fact that rising borrowing costs were preceded by robust nominal property appreciation. By late 2022, mortgage holders faced some of the steepest rate increases in decades, yet house price growth was 20% higher than the pre-pandemic period. This environment uncovers a novel configuration – the usual dampening of demand from higher borrowing costs is partly offset by increased borrowing against robust collateral values experienced since the previous refinancing event.

Third, we exploit the design of mortgage flexibility offers in the UK which allows us to separate it from any changes households make after their new interest rate is realised. Mortgage flexibility decisions are agreed at the remortgage application stage, typically 3–6 months before the refinancing event when new fixed-term contracts are locked in. Households observe the realised interest rate shock only at the refinancing date when new contracts start. The delay between application and refinancing helps us separate the decision to use flexibility from subsequent consumption adjustments. We show that households do not behave differently in anticipation of new mortgage contract terms, in line with the literature. In addition, we compare treated and controls who make the same mortgage flexibility choices, to minimise any systematic differences between households. As a result, we isolate the effect of the rising mortgage rates on consumption, debt and savings, conditional on a specific type of mortgage flexibility choice.

Finally, we use a novel data set from ExactOne’s app called ClearScore, which offers budgeting advice based on up-to-date timely household transactions. We combine this with UK loan-level mortgages from the Product Sales Database (PSD) to obtain a near complete view of UK household spending, unsecured debt and liquid savings. Our sample follows around 60,000 users between 2021–23. We show that our matched ExactOne-PSD sample is representative across borrowers’ age, regional distribution, debt characteristics, savings and expenditure when compared to the universe of mortgages available in PSD and data from the Office of National Statistics.

The impact of higher mortgage payments on household finances depends greatly on mortgage flexibility

Monthly mortgage payments increased by around 20% on average during the hiking cycle. In response, aggregate spending across all affected households dropped temporarily by about 3% at the refinancing event compared to control units who refinanced before the hiking cycle (red line, chart 1a). However, household reactions to higher interest rates depended on their take-up of mortgage flexibility. Households who did not modify their loans reduced spending by nearly 5% for six months relative to controls (blue line, chart 1a). In contrast, households who used mortgage flexibility (around 30% of our sample) temporarily increased spending by 5% and consolidated their unsecured debt portfolios compared to control units who refinanced before the policy hiking cycle and used similar mortgage flexibility measures (green lines, Chart 1a and b). We show that take-up of mortgage flexibility is strongly correlated with wealthier hand-to-mouth borrowers – ie those having higher property wealth, higher income and lower savings.

Chart 1 also shows that prior to the refinancing event (at time 0), there is no difference in behaviours between treated and controls, alleviating concerns around anticipation effects, especially given that mortgage flexibility choices are decided in advance of the refinancing event.

Chart 1: Impact of loan adjustments at refinancing

| (a) Total non-housing spending | (b) Unsecured debt repayments |

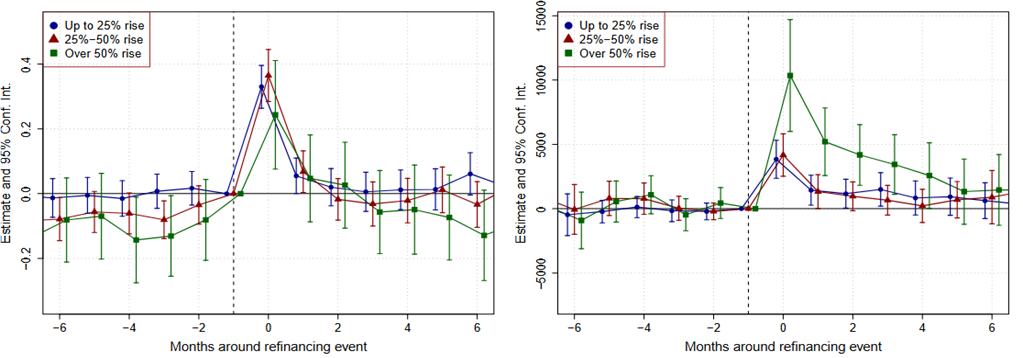

Heterogeneity across collateral-driven borrowing

We find a strong association between collateral-driven borrowing and households’ balance sheet readjustments. For instance, the greater the property price gains since the previous refinancing event, the larger the home equity extraction and the subsequent spending and saving buffers that households build (red and green lines, Chart 2). This illustrates how leveraging house price appreciation at refinancing can help household build financial resilience against shocks. Indeed, our paper shows that an important factor in the decision of how much home equity to extract is having low liquid savings.

Chart 2: Impact of housing collateral appreciation for the borrowing and spending behaviour of households extracting equity

| (a) Total non-housing spending | (b) Saving balances |

In addition, we find that extending mortgage terms at refinancing amplifies the link between collateral-driven borrowing and spending. By borrowing more against their home, households are likely to see increases in their monthly mortgage repayments beyond the effects of the tightening cycle. Extending the repayment period helps spread the cost over time, making payments more manageable. Households who both extract equity and increase mortgage terms simultaneously, are able to increase their spending on impact by nearly 20% (blue line, Chart 3a) relative to control units. In contrast, borrowing more without extending terms leads to spending responses not statistically different from control units, suggesting that equity extraction was used to keep spending unchanged – ie smooth the shock to mortgage repayments (red line, Chart 3a). This result is driven by higher borrowing ability when both mortgage flexibility measures are used. Specifically, households are able to borrow £15,000 more if they also extend mortgage terms at refinancing, compared to the average equity extractor in the control group (blue line, Chart 3b).

Chart 3: Impact of equity extraction and term extensions at refinancing

| (a) Total non-housing spending for equity extractors | (b) Equity extraction |

What does this all mean for policy?

Our findings reveal that during periods of rising interest rates, about one-in-three households rely on additional borrowing and on extending loan repayment terms, in order to smooth the impact of higher monthly mortgage repayments. Those not exploiting these flexibility measures when refinancing, reduced their spending materially when faced with a rise in borrowing costs. While mortgage flexibility has dampened the transmission of monetary policy tightening for some groups, it also enhanced the financial resilience of mortgagors to negative income shocks. Future research could look into their cyclicality: do mortgage term extensions and equity extractions lead to greater debt persistence over the life cycle, impacting households’ future financial outcomes, or are they reversed in subsequent periods?

Philippe Bracke and Matt Everitt work in the Bank’s Advanced Analytics Division, and Martina Fazio and Alexandra Varadi work in the Bank’s Macrofinancial Risk Division.

If you want to get in touch, please email us at [email protected] or leave a comment below.

Comments will only appear once approved by a moderator, and are only published where a full name is supplied. Bank Underground is a blog for Bank of England staff to share views that challenge – or support – prevailing policy orthodoxies. The views expressed here are those of the authors, and are not necessarily those of the Bank of England, or its policy committees.

Share the post “When mortgage flexibility meets monetary policy tightening: heterogeneous impacts on spending and debt”

Publisher: Source link

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}