Mortgage delinquency rates were up in the fourth quarter, with sharper increases in areas with rising unemployment rates and falling home prices, a new industry report shows.

Processing Content

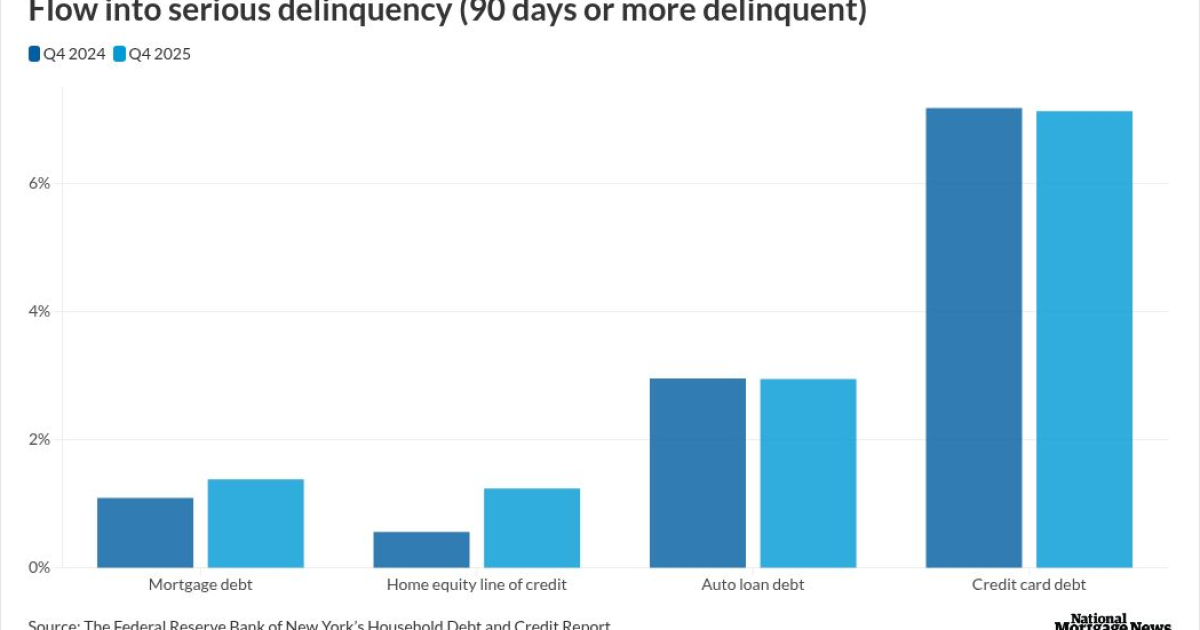

While credit card and loan delinquency rates have mellowed, albeit at elevated rates, mortgage delinquency rates

“It is kind of surprising given the underwriting over the last [few] years,” said a New York Fed researchers, on a conference call Tuesday. “Mortgages are all associated with very high credit scores and high income, but we are seeing … rising delinquencies amongst lower income groups, so again, evidence of a K-shaped economy.”

Borrowers in the lowest-income zip codes have seen their 90-days-or-more delinquency rates soar since 2021, jumping from about 0.5% to nearly 3%, while borrowers in the highest-income areas maintained delinquency rates below 1%. Middle-income zip codes experienced rising delinquency rates as well, but not as steep as those with lower incomes, the data showed.

The report also found a correlation between growing unemployment and delinquency rates.

The national unemployment rate dropped to 3.4% in April 2023 and has increased roughly 1 percentage point since then. Regionally, unemployment rates rose in two-thirds of counties, and 5% of Americans live in one where rates climbed more than 1.6 percentage points. These counties were disproportionally located in Florida and Minnesota, the report said.

Counties that experienced the largest

“There’s some interesting differences there between loan types,” NY Fed researchers said on the call. “In August of last year, we did a blog post where we showed the increase is much, much higher amongst [Federal Housing Administration] mortgages, and so again, consistent with our blog post this time, which shows that these delinquency rates and the increases are highly concentrated in low income areas and also areas where home prices have been falling.”

Home prices were

Overall, aggregate household debt balances climbed $191 billion to $18.8 trillion in the fourth quarter, a 32.4% jump from the end of 2019. Mortgage balances grew $98 billion to $13.2 trillion, while credit card debt expanded by $44 billion to $1.28 trillion, the report found.

Home equity lines of credit were also up by $12 billion, as HELOC balances have been increasing since 2022, which is notable because they were in a long-term decline since 2009, said reseachers on the call.

Publisher: Source link